What Is Ahead for the Market Post the Middle East Conflict Eases, and the Future of Commodities?

Source: Kapitales Research

Executive Introduction

Global financial markets are entering a new phase as easing Middle East tensions reduce geopolitical risks and investors shift their attention towards economic fundamentals. The decline in oil's geopolitical risk premium, coupled with weaker-than-expected U.S. employment data, has altered expectations for Federal Reserve policy and created diverging trends across commodity markets. While crude oil prices remain under pressure due to improving global supply conditions and easing geopolitical risk premiums, precious metals have regained momentum as softer U.S. economic data has reduced expectations for additional Federal Reserve rate hikes, weakening the U.S. dollar and supporting bullion. Looking ahead, commodity markets are expected to be driven increasingly by macroeconomic fundamentals, including global economic growth, inflation trends, central bank policy, supply-demand dynamics and Chinese industrial demand, rather than geopolitical developments alone.

Middle East Tensions Ease, Shifting Market Focus

The de-escalation of tensions between the United States and Iran has significantly reduced concerns over disruptions to global energy supplies. Markets have largely unwound the geopolitical premium that supported crude oil prices during the conflict, allowing investors to refocus on broader economic conditions.

While negotiations between Washington and Tehran continue, concerns regarding the Strait of Hormuz have diminished compared to previous months. Nonetheless, developments in the region remain a significant risk factor that could quickly impact energy markets if geopolitical tensions resurface.

Oil Prices Face Pressure as Supply Outlook Improves

Crude oil prices have softened as improving physical supply conditions outweigh geopolitical concerns. Recovering crude exports through the Strait of Hormuz, Saudi Arabia's exports returning to nearly 90% of pre-conflict levels, and expectations of ample near-term supplies have weighed on market sentiment.

Crude oil remains under pressure as improving supply conditions and easing geopolitical risk premiums weigh on prices. Meanwhile, China’s independent refiners have increased crude purchases to benefit from lower prices and more competitive pricing from Middle Eastern producers. However, Iran continues to face export challenges, with a sizeable volume of crude reportedly held in floating storage awaiting buyers.

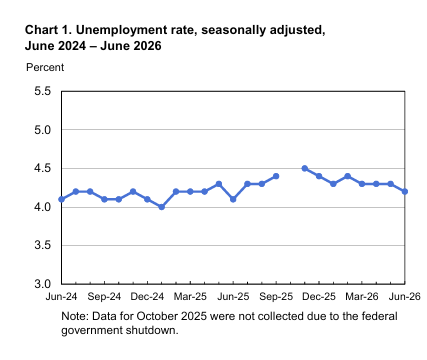

THE EMPLOYMENT SITUATION — JUNE 2026

Source: U.S. Bureau of Labor Statistics

Softer U.S. Labour Data Revives Gold

The latest U.S. labour market report provided fresh support for precious metals. Nonfarm payrolls increased by only 57,000 jobs in June, substantially below market expectations of 114,000, while payroll figures for April and May were revised lower by a combined 74,000 jobs.

Although the unemployment rate edged lower to 4.2%, the labour force participation rate declined to 61.5%, suggesting that the improvement was driven partly by fewer people participating in the workforce rather than stronger hiring activity. The softer labour market has led investors to reassess the outlook for U.S. monetary policy. Before the June employment report, markets were pricing in roughly a 50% probability of a Federal Reserve rate hike at its September meeting. However, weaker payroll growth has reduced expectations for further policy tightening. While the Federal Reserve left its benchmark interest rate unchanged at 3.50%–3.75% in June, its latest economic projections continue to indicate that one additional rate increase later this year remains possible if inflationary pressures persist.

As a result, spot gold recovered to approximately US$4,128.74 per ounce, while gold futures climbed to around US$4,142.25 per ounce, placing bullion on track for its first weekly gain in five weeks.

Federal Reserve Outlook Supports Precious Metals

The weaker employment report has reduced expectations for aggressive monetary tightening, leading to lower Treasury yields and a softer U.S. dollar. Both developments have improved the investment case for gold by reducing the opportunity cost of holding non-yielding assets.

Nevertheless, the Federal Reserve remains data dependent. Inflation, employment, consumer spending, and broader economic activity will continue to determine the future direction of interest rates. Consequently, commodity markets are expected to remain highly responsive to upcoming economic releases.

The Future of Commodities

As geopolitical risks gradually fade, commodity markets are transitioning toward a fundamentals-driven environment.

Oil prices are likely to remain influenced by global supply growth, OPEC+ production decisions, Chinese demand and inventory levels. Unless fresh geopolitical disruptions emerge, abundant supply could continue limiting upside in crude prices.

Gold is likely to remain well supported if expectations for a less restrictive Federal Reserve policy persist, supported by lower bond yields, a softer U.S. dollar and continued macroeconomic uncertainty that reinforces demand for defensive assets. Meanwhile, industrial metals such as copper and aluminium are expected to become increasingly dependent on infrastructure spending, manufacturing activity and China's economic recovery. Agricultural commodities will remain sensitive to weather patterns, trade flows and global food demand.

Overall, macroeconomic conditions are expected to become the dominant driver of commodity prices during the second half of 2026.

What Australian Investors Should Do

Prioritise investment in financially strong ASX-listed commodity producers with diversified operations and disciplined capital allocation.

Closely monitor U.S. inflation, employment and Federal Reserve policy announcements, as these remain key drivers of commodity prices.

Track developments in OPEC+ production policy and negotiations involving the Middle East, particularly around the Strait of Hormuz.

Consider diversified exposure across gold, energy and industrial metals rather than concentrating investments in a single commodity.

Watch Chinese economic indicators closely, as infrastructure spending and industrial activity will significantly influence demand for metals and energy.

Review currency movements, particularly the U.S. dollar, as exchange rate fluctuations continue to affect commodity pricing and Australian resource stocks.

Maintain a long-term investment approach by focusing on company fundamentals instead of reacting to short-term geopolitical headlines.

Key Risks to Monitor

Despite the recent easing of geopolitical tensions, the outlook for commodity markets remains subject to several important risks. Any deterioration in U.S.-Iran negotiations, renewed disruptions to shipping through the Strait of Hormuz, or unexpected changes in OPEC+ production policy could tighten global crude supplies and reignite volatility in oil prices. Conversely, stronger-than-expected U.S. economic data or persistent inflationary pressures could reinforce expectations of tighter Federal Reserve monetary policy, supporting the U.S. dollar and increasing bond yields, which may weigh on gold prices. Investors should also closely monitor the pace of China's economic recovery, global manufacturing activity, industrial demand and international trade developments, as these factors are expected to play a pivotal role in shaping commodity demand and price trends over the medium term.

Conclusion

The easing of Middle East tensions marks an important transition for global financial markets, shifting investor attention from geopolitical uncertainty toward economic fundamentals and monetary policy. While improving global supply conditions and easing geopolitical tensions continue to weigh on crude oil prices, gold has regained some momentum after softer U.S. labour market data modestly reduced expectations of a more hawkish Federal Reserve stance, supporting lower bond yields and improving sentiment toward bullion. Looking ahead, commodity markets are expected to become increasingly driven by global growth, inflation trends, central bank decisions and supply-demand dynamics. For Australian investors, maintaining diversified exposure to fundamentally strong resource companies while closely monitoring macroeconomic developments is likely to remain the most prudent investment strategy as markets enter the next phase of the commodity cycle.

Disclaimer for Kapitales Research

The materials provided by Kapitales Research, including articles, news, data, reports, opinions, images, charts, and videos ("Content"), are intended for personal, non-commercial use only. The primary goal of this Content is to educate and inform readers. This Content is not meant to offer financial advice, nor does it include any recommendation or opinion that should be relied upon for making financial decisions. Certain Content on this platform may be sponsored or unsponsored, but it does not serve as a solicitation or endorsement to buy, sell, or hold any securities, nor does it encourage any specific investment activities. Kapitales Research is not authorized to provide investment advice, and we strongly advise users to seek guidance from a qualified financial professional, such as a financial advisor or stockbroker, before making any investment choices. Kapitales Research disclaims all liability for any direct, indirect, incidental, or consequential damages arising from the use of the Content, which is provided without any warranties. The opinions expressed by contributors or guests are their own and do not necessarily reflect the views of Kapitales Research. Media such as images or music used on this platform are either owned by Kapitales Research, sourced through paid subscriptions, or believed to be in the public domain. We have made reasonable efforts to credit sources where appropriate. Kapitales Research does not claim ownership of any third-party media unless explicitly stated otherwise.

Customer Notice:

Nextgen Global Services Pty Ltd trading as Kapitales Research (ABN 89 652 632 561) is a Corporate Authorised Representative (CAR No. 1293674) of Enva Australia Pty Ltd (AFSL 424494). The information contained in this website is general information only. Any advice is general advice only. No consideration has been given or will be given to the individual investment objectives, financial situation or needs of any particular person. The decision to invest or trade and the method selected is a personal decision and involves an inherent level of risk, and you must undertake your own investigations and obtain your own advice regarding the suitability of this product for your circumstances. Please be aware that all trading activity is subject to both profit & loss and may not be suitable for you. The past performance of this product is not and should not be taken as an indication of future performance.

Disclosure: The information mentioned above has been sourced from the company reports and a third-party database, i.e. Koyfin. Investors are advised to use strict stop-loss to protect their investments in case of any unfavorable/uncertain market events.

Kapitales Research, Level 13, Suite 1A, 465 Victoria Ave, Chatswood, NSW 2067, Australia | 1800 005 780 | info@kapitales.com.au

x

Daily Dose of Buy, Sell & Hold recommendations before the market opens.

Start Your 7 Days Free Trial Now!

We use cookies to help us improve, promote, and protect our services.

By continuing to use this site, we assume you consent to this.

Read our

Privacy Policy

and

Terms & Conditions

What Is Ahead for the Market Post the Middle East Conflict Eases, and the Future of Commodities?

Executive Introduction

Global financial markets are entering a new phase as easing Middle East tensions reduce geopolitical risks and investors shift their attention towards economic fundamentals. The decline in oil's geopolitical risk premium, coupled with weaker-than-expected U.S. employment data, has altered expectations for Federal Reserve policy and created diverging trends across commodity markets. While crude oil prices remain under pressure due to improving global supply conditions and easing geopolitical risk premiums, precious metals have regained momentum as softer U.S. economic data has reduced expectations for additional Federal Reserve rate hikes, weakening the U.S. dollar and supporting bullion. Looking ahead, commodity markets are expected to be driven increasingly by macroeconomic fundamentals, including global economic growth, inflation trends, central bank policy, supply-demand dynamics and Chinese industrial demand, rather than geopolitical developments alone.

Middle East Tensions Ease, Shifting Market Focus

The de-escalation of tensions between the United States and Iran has significantly reduced concerns over disruptions to global energy supplies. Markets have largely unwound the geopolitical premium that supported crude oil prices during the conflict, allowing investors to refocus on broader economic conditions.

While negotiations between Washington and Tehran continue, concerns regarding the Strait of Hormuz have diminished compared to previous months. Nonetheless, developments in the region remain a significant risk factor that could quickly impact energy markets if geopolitical tensions resurface.

Oil Prices Face Pressure as Supply Outlook Improves

Crude oil prices have softened as improving physical supply conditions outweigh geopolitical concerns. Recovering crude exports through the Strait of Hormuz, Saudi Arabia's exports returning to nearly 90% of pre-conflict levels, and expectations of ample near-term supplies have weighed on market sentiment.

Crude oil remains under pressure as improving supply conditions and easing geopolitical risk premiums weigh on prices. Meanwhile, China’s independent refiners have increased crude purchases to benefit from lower prices and more competitive pricing from Middle Eastern producers. However, Iran continues to face export challenges, with a sizeable volume of crude reportedly held in floating storage awaiting buyers.

THE EMPLOYMENT SITUATION — JUNE 2026

Source: U.S. Bureau of Labor Statistics

Softer U.S. Labour Data Revives Gold

The latest U.S. labour market report provided fresh support for precious metals. Nonfarm payrolls increased by only 57,000 jobs in June, substantially below market expectations of 114,000, while payroll figures for April and May were revised lower by a combined 74,000 jobs.

Although the unemployment rate edged lower to 4.2%, the labour force participation rate declined to 61.5%, suggesting that the improvement was driven partly by fewer people participating in the workforce rather than stronger hiring activity. The softer labour market has led investors to reassess the outlook for U.S. monetary policy. Before the June employment report, markets were pricing in roughly a 50% probability of a Federal Reserve rate hike at its September meeting. However, weaker payroll growth has reduced expectations for further policy tightening. While the Federal Reserve left its benchmark interest rate unchanged at 3.50%–3.75% in June, its latest economic projections continue to indicate that one additional rate increase later this year remains possible if inflationary pressures persist.

As a result, spot gold recovered to approximately US$4,128.74 per ounce, while gold futures climbed to around US$4,142.25 per ounce, placing bullion on track for its first weekly gain in five weeks.

Federal Reserve Outlook Supports Precious Metals

The weaker employment report has reduced expectations for aggressive monetary tightening, leading to lower Treasury yields and a softer U.S. dollar. Both developments have improved the investment case for gold by reducing the opportunity cost of holding non-yielding assets.

Nevertheless, the Federal Reserve remains data dependent. Inflation, employment, consumer spending, and broader economic activity will continue to determine the future direction of interest rates. Consequently, commodity markets are expected to remain highly responsive to upcoming economic releases.

The Future of Commodities

As geopolitical risks gradually fade, commodity markets are transitioning toward a fundamentals-driven environment.

Oil prices are likely to remain influenced by global supply growth, OPEC+ production decisions, Chinese demand and inventory levels. Unless fresh geopolitical disruptions emerge, abundant supply could continue limiting upside in crude prices.

Gold is likely to remain well supported if expectations for a less restrictive Federal Reserve policy persist, supported by lower bond yields, a softer U.S. dollar and continued macroeconomic uncertainty that reinforces demand for defensive assets. Meanwhile, industrial metals such as copper and aluminium are expected to become increasingly dependent on infrastructure spending, manufacturing activity and China's economic recovery. Agricultural commodities will remain sensitive to weather patterns, trade flows and global food demand.

Overall, macroeconomic conditions are expected to become the dominant driver of commodity prices during the second half of 2026.

What Australian Investors Should Do

Key Risks to Monitor

Despite the recent easing of geopolitical tensions, the outlook for commodity markets remains subject to several important risks. Any deterioration in U.S.-Iran negotiations, renewed disruptions to shipping through the Strait of Hormuz, or unexpected changes in OPEC+ production policy could tighten global crude supplies and reignite volatility in oil prices. Conversely, stronger-than-expected U.S. economic data or persistent inflationary pressures could reinforce expectations of tighter Federal Reserve monetary policy, supporting the U.S. dollar and increasing bond yields, which may weigh on gold prices. Investors should also closely monitor the pace of China's economic recovery, global manufacturing activity, industrial demand and international trade developments, as these factors are expected to play a pivotal role in shaping commodity demand and price trends over the medium term.

Conclusion

The easing of Middle East tensions marks an important transition for global financial markets, shifting investor attention from geopolitical uncertainty toward economic fundamentals and monetary policy. While improving global supply conditions and easing geopolitical tensions continue to weigh on crude oil prices, gold has regained some momentum after softer U.S. labour market data modestly reduced expectations of a more hawkish Federal Reserve stance, supporting lower bond yields and improving sentiment toward bullion. Looking ahead, commodity markets are expected to become increasingly driven by global growth, inflation trends, central bank decisions and supply-demand dynamics. For Australian investors, maintaining diversified exposure to fundamentally strong resource companies while closely monitoring macroeconomic developments is likely to remain the most prudent investment strategy as markets enter the next phase of the commodity cycle.

Disclaimer for Kapitales Research

The materials provided by Kapitales Research, including articles, news, data, reports, opinions, images, charts, and videos ("Content"), are intended for personal, non-commercial use only. The primary goal of this Content is to educate and inform readers. This Content is not meant to offer financial advice, nor does it include any recommendation or opinion that should be relied upon for making financial decisions. Certain Content on this platform may be sponsored or unsponsored, but it does not serve as a solicitation or endorsement to buy, sell, or hold any securities, nor does it encourage any specific investment activities. Kapitales Research is not authorized to provide investment advice, and we strongly advise users to seek guidance from a qualified financial professional, such as a financial advisor or stockbroker, before making any investment choices. Kapitales Research disclaims all liability for any direct, indirect, incidental, or consequential damages arising from the use of the Content, which is provided without any warranties. The opinions expressed by contributors or guests are their own and do not necessarily reflect the views of Kapitales Research. Media such as images or music used on this platform are either owned by Kapitales Research, sourced through paid subscriptions, or believed to be in the public domain. We have made reasonable efforts to credit sources where appropriate. Kapitales Research does not claim ownership of any third-party media unless explicitly stated otherwise.

Customer Notice:

Nextgen Global Services Pty Ltd trading as Kapitales Research (ABN 89 652 632 561) is a Corporate Authorised Representative (CAR No. 1293674) of Enva Australia Pty Ltd (AFSL 424494). The information contained in this website is general information only. Any advice is general advice only. No consideration has been given or will be given to the individual investment objectives, financial situation or needs of any particular person. The decision to invest or trade and the method selected is a personal decision and involves an inherent level of risk, and you must undertake your own investigations and obtain your own advice regarding the suitability of this product for your circumstances. Please be aware that all trading activity is subject to both profit & loss and may not be suitable for you. The past performance of this product is not and should not be taken as an indication of future performance.

Disclosure: The information mentioned above has been sourced from the company reports and a third-party database, i.e. Koyfin. Investors are advised to use strict stop-loss to protect their investments in case of any unfavorable/uncertain market events.

Kapitales Research, Level 13, Suite 1A, 465 Victoria Ave, Chatswood, NSW 2067, Australia | 1800 005 780 | info@kapitales.com.au